The June sales pace extended the recovery that began in May, though the first-half total stayed below a 2025 stretch inflated by pre-tariff buying.

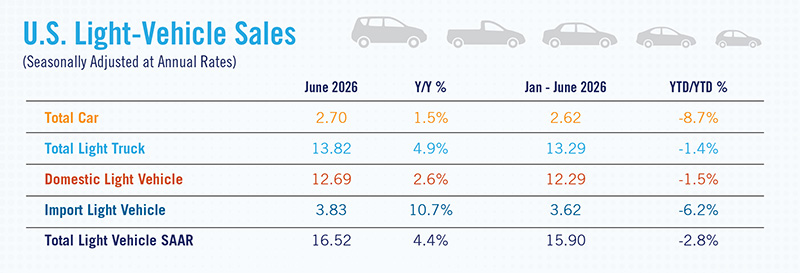

New light-vehicle sales reached a seasonally adjusted annual rate (SAAR) of 16.52 million units in June 2026, up 4.4% from June 2025, according to the latest National Automobile Dealers Association (NADA) Market Beat report authored by chief economist Patrick Manzi. It was the second consecutive month of year-over-year gains, following the 3.1% increase in May that broke an eight-month run of declines.

Year to date through June, the new light-vehicle SAAR stood at 15.9 million units, down 2.8% from the same period in 2025. The first half of 2025 included significant pull-ahead volume as consumers bought vehicles before tariffs on imported autos and auto parts took effect, and NADA cautioned that the elevated year-ago base should be kept in mind when comparing the two periods.

For collision repair operators and auto insurance claims professionals, the shifts in the sales mix beneath the headline pace carry more weight than the SAAR itself. Hybrid penetration keeps climbing, battery electric vehicle demand keeps softening and crossovers and pickups continue to dominate segment share — all factors that shape the vehicles entering collision repair facilities and the parts and procedures insurers will pay for in the months ahead.

NADA held its full-year outlook steady. “Looking ahead to the rest of 2026, our forecast for new light-vehicle sales remains at 16.0 million units,” Manzi wrote in the report.

Conventional hybrids remained the market’s standout. Hybrid sales through the first half of 2026 totaled 1.21 million units, up 19.4% from the first half of 2025, and hybrids reached 15.4% of the market over that span, an increase of 2.9 percentage points from a year earlier.

“Sales of conventional hybrid vehicles continue to be red hot,” Manzi wrote.

Battery electric vehicles moved the other way. BEV sales fell 25.1% year over year through the first half of 2026, and BEV market share declined 1.7 percentage points from the same period in 2025. In June, plug-in hybrids accounted for 1.2% of the market, fuel cell vehicles for 0.0% and internal combustion engines still powered 77.6% of new light-vehicle sales.

Rising prices and payments continued to narrow the active buying pool. JD Power estimated the average monthly payment on a new-vehicle finance contract at $813 in June, up 3.4% year over year and the highest ever recorded for any June. OEM incentive spending also increased, with JD Power estimating average incentive spending per unit at $3,217 in June, up 12.7% from a year earlier.

More buyers stretched their loan terms to keep payments manageable. JD Power estimated that 13.6% of new-vehicle loans now carry terms of 84 months or longer, up from 13.4% in May.

USMCA Left Unrenewed as Auto Groups Seek Extension

Manzi’s report noted that the United States will not renew the U.S.-Mexico-Canada Agreement in its current form. Negotiations between the United States and Mexico are set to continue through July 20, with no date yet set for talks between the United States and Canada.

As CollisionWeek reported, U.S. Trade Representative Jamieson Greer said after the July 1 joint review that Washington would not renew the pact in its current form, though the agreement remains in force. NADA was among a coalition of automotive trade groups that urged the three governments to reach an extension rather than let the agreement’s terms lapse. The pact’s automotive rules of origin, along with the Section 232 tariffs layered atop them, govern a supply chain in which Canada and Mexico together account for roughly 30% of the auto parts used in the United States.

Segment and Manufacturer Share

Crossovers held the largest segment share in June at 49.0%, followed by pickups at 18.8%, SUVs at 10.6%, small cars at 7.3%, mid-size and large cars at 6.8%, vans at 4.9% and luxury cars at 2.5%.

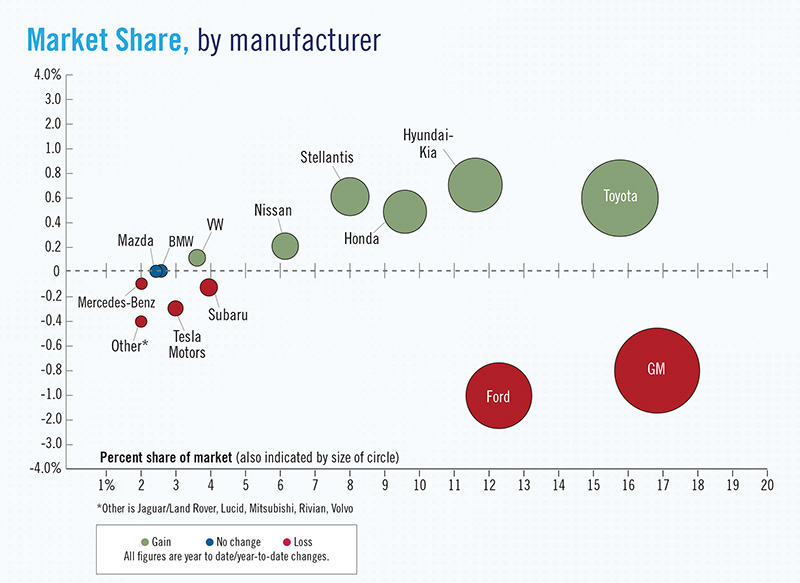

Toyota, GM and Ford continued to hold the largest U.S. market shares. On a year-to-date basis, Toyota, Stellantis, Honda, Nissan, Hyundai-Kia, BMW, Volkswagen and Mazda posted share gains, while GM, Ford, Tesla, Subaru and Mercedes-Benz lost ground, as did an “Other” group comprising Jaguar/Land Rover, Lucid, Mitsubishi, Rivian and Volvo. Volkswagen and Mazda flipped to gainers after losing year-to-date share in the April report.

Total light-vehicle SAAR for June was 16.52 million units, up 4.4% year over year. Total car SAAR stood at 2.70 million units, up 1.5%, while total light-truck SAAR reached 13.82 million units, up 4.9%. Domestic light-vehicle SAAR was 12.69 million units, up 2.6%, and import light-vehicle SAAR totaled 3.83 million units, up 10.7%. The year-to-date picture stayed weaker: car SAAR was down 8.7% and import SAAR down 6.2%, against smaller declines of 1.4% for light trucks and 1.5% for domestic vehicles.

Leave a Reply

You must be logged in to post a comment.