Reports year-over-year market gains and continued recovery in Refinish and Mobility coatings segments.

Axalta Coating Systems Ltd. (NYSE:AXTA) reported third quarter net sales of $1,238.7 million increased 13.8% year-over-year, after the negative 6.3% foreign currency impact. The strong year-over-year growth was driven by 9.7% higher average price-mix, a 1.6% M&A benefit and 8.8% better volumes. Performance Coatings net sales increased 7.5% year-over-year, driven by constant currency growth of 19.9% in Refinish and 7.1% in Industrial. Mobility Coatings net sales increased 29.5% supported by a recovery in global auto production from the severe supply constraints in the prior-year period.

Volume increased 8.8% driven largely by market recovery in both Refinish and Mobility despite impacts of the Russia- Ukraine conflict, China COVID-19 lockdowns, and Industrial EMEA slowing. The company Axalta realized a 9.7% price-mix growth with contributions from every end-market and 2.5% sequential price-mix growth reflects continued pricing momentum

Income from operations for Q3 2022 totaled $123.5 million versus $124.7 million in Q3 2021. Net income to common shareholders was $62.4 million for the quarter compared with $69.1 million in Q3 2021. Diluted earnings per share was $0.28 compared with $0.30 in Q3 2021. Q3 2022 benefited from robust sales growth, including significant realized pricing gains and volume improvement; however, operating income was negatively impacted by continued variable raw material inflation, and elevated logistics, energy and labor expenses. In addition, foreign currency headwinds, the Russia-Ukraine conflict and COVID-19 lockdowns in China represented a combined ~$16 million headwind to income from operations in the quarter.

Rakesh Sachdev, Axalta’s interim CEO and President, commented, “I am pleased that we were able to report earnings within our stated guidance range despite acute currency and inflationary headwinds plus pockets of softening regional demand. Our resilient third quarter performance can be attributed to the prioritization of price to offset variable cost inflation, as well as continued market recovery in our Refinish and Light Vehicle end-markets. New customer wins across the portfolio supported volume growth and again highlighted our customers’ continued preference for our industry-leading products and services. The third quarter also represented an inflection point in our price-cost trajectory as we more than offset year-over-year variable cost inflation for the first time since the current unprecedented inflationary environment began in mid-2021. Our teams are taking the steps necessary to recapture the value provided by our products and services to our partners, but more is needed for us to return to pre-COVID levels of profitability.”

Mr. Sachdev continued, “Enhancing our profitability is among my highest near-term strategic imperatives. Successful day-to- day execution is fundamental to achieving our long-term goals, which will be realized through driving improved operational performance and productivity. We have a great leadership team ready to tackle these objectives. I believe we can accelerate a return to pre-COVID profitability on our pathway to sustained growth.”

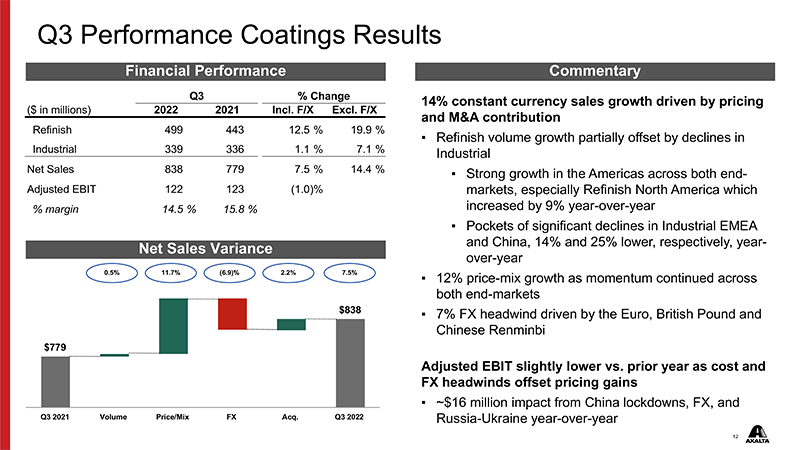

Refinish net sales increased 12.5% to $498.7 million (19.9% ex-FX) in Q3 2022, including a 4.3% increase in volume and a 3.9% contribution from M&A, partially offset by a foreign exchange headwind of 7.4%. Refinish volume growth was very strong in the Americas and stable in China and in EMEA year-over-year. The market recovery is steadily progressing with improvement in key metrics such as office occupancy and road congestion. Refinish again drove above-market volume growth with several notable MSO wins in the quarter alongside an increase in points of distribution. Sequentially, volumes declined 4.4% consistent with seasonal factors and in line with prior expectations. Price-mix was 11.7% higher year-over-year, which more than offset the impact of continued variable cost inflation.

Sean Lannon, Axalta’s Chief Financial Officer, commented, “Overall demand growth in the third quarter was robust especially within Refinish and Mobility Coatings where we continue to see recovery; yet, slower regional economic activity was evident in select geographies, namely in the EMEA and Chinese Industrial markets. In these areas, sales softened considerably beginning in Q2, and continued through Q3, driven by slower than anticipated post-COVID-19 lockdown recovery in China and EMEA macroeconomic and energy headwinds, which we expect to continue through the fourth quarter. Currently, the slowdown seems to be fairly concentrated within Industrial. We have layered in the broader geographic weakness into our Q4 outlook, which also reflects substantial FX headwinds and minimal change in the sequential quarter-over-quarter cost environment. We believe that the resiliency of our Refinish end-market, deferred demand in both Commercial Vehicle and Light Vehicle and company-wide pricing momentum are natural hedges if macros step lower.”